According to Accenture, Artificial Intelligence (AI) is being used to redefine the banking experience and business economics like the computer and Internet did before. The possibilities are both endless and already limitedly proven.

Artificial intelligence (AI) and machine learning (ML) are transforming the lending ecosystem by leveraging vast data to understand consumer trends and patterns and helping lenders make quick and intelligent decisions. These new-age technologies help engage each customer individually across the customer

lifecycle, from acquisition, upsell, and cross-sell to risk segmentation and debt collection. AI/ML enables lenders, like you, to provide a digitally smart experience to your customers through intelligent underwriting, real-time intelligent decision-making, and offering products that suit customers’ evolving needs. It not only helps you predict those prospects who have a high possibility to convert but also safeguards you from defaulters.

Let’s understand the significance of AI/ML in the lending space:

Customer Acquisition

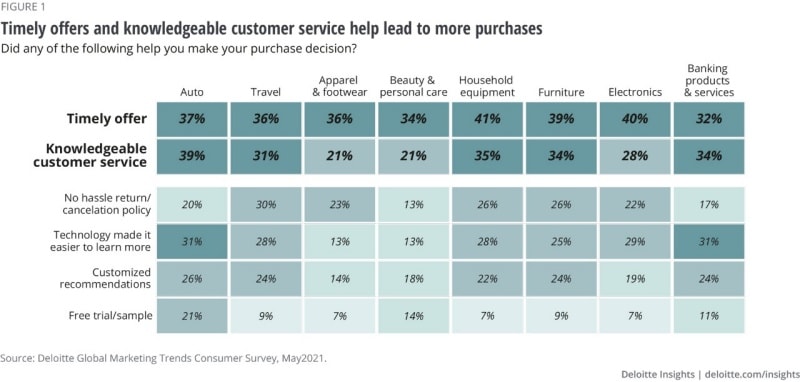

According to a 2021 survey by Deloitte, 32% of banking products and services consumers said timely offers help them make a purchase decision, and 34% said knowledgeable customer service helped them in doing so.

AI helps predict customers, who have the propensity to take up loans and who do not. If you go through the entire loan initiation and execution processes but are unable to convert the prospect into a customer, it can adversely impact you. AI/ML can screen all applications, analyze data, and provide insights into the most promising prospects. Based on the results, you can plan a relevant and timely campaign, and offer personalized lending rates, thereby increasing conversions.

Credit Risk Assessment and Credit Decisioning

By leveraging the AI-powered lending solution, you can generate prompt credit decisions for corporate clients, mini, small, and medium-size enterprises, retailers, or customers looking for personal loans.

The continuous learning model segments the customers to better understand their risk profile. AI-powered decision-making processes help underwriters approve and reject loans based on predictive scores, with only deviations to the outliers. It helps you offer optimal loan amounts with risk-based pricing to the right customers and reduces non-performing loans (NPL) on accurate predictive risk models.

Loan Payment Prediction

Modern customers are constantly looking to reduce their interest burden and channel more capital toward investments. Pre-pay loans or transfer loan balances to a competitor can impact lenders’ revenue prediction and working capital. Once the loan is approved, AI helps you strategically identify those customers who are likely to pre-pay and adopt a differentiation strategy to retain them and upsell/cross-sell to them.

Loan Default Prediction

Per McKinsey & Company report of 2021, AI-first banks are engaging with clients proactively to help them keep up with payments and work more closely with clients who encounter difficulties.

A lender’s NPA (non-performing asset) is a closely watched figure, which helps you review and fine-tune your credit assessment strategy. To predict defaulters, AI is used to review customers’ financial health based on credit rating, past payment history, etc. This allows banks to engage, communicate and work towards loan restructuring to reduce default. Additionally, lenders’ exposure to default risk can be tracked to predict yearly losses accurately.

Debt Collections

AI allows you to define a debt collection strategy from the loan origination stage by predicting customers who are most likely to pay the debt. Scores can determine your collection strategies, which also predict your collection costs. Lenders can accurately predict collections, plan their budgets, and forecast incentives to be paid out to debt collectors. AI can help you predict the customers most likely to repay their debts. Scoring can help you plan your budget and make strategies to maximize recoveries and reduce costs.

Cost Minimization

AI-powered business models require minimal human intervention that significantly reduces the cost of document handling. It can analyze the incoming applications, identify the concerned areas, verify, and evaluate virtually, and send it to straight-through processing if it meets all the required criteria. In case any fraudulent activity is tracked in the pattern, underwriters are instantly alerted to take immediate steps of action.

In a Nutshell

According to RESEARCH AND MARKETS, The global digital lending platform market size is expected to reach USD 26.08 billion by 2028, registering a CAGR of 24.0% from 2021 to 2028.

The given data and the stated points clearly indicate that AI-powered lending solution is the need of the hour for new-age lenders to remain current, competitive, and future-ready.

(The author is Mr. Rajan Nagina, Head of AI Practice, Newgen Software and the views expressed in this article are his own)

{kind=link}